The Trillion-Dollar Arbitrage - Why Distressed Affordable Housing is the Best Investment of the Decade

The Trillion-Dollar Arbitrage - Why Distressed Affordable Housing is the Best Investment of the Decade

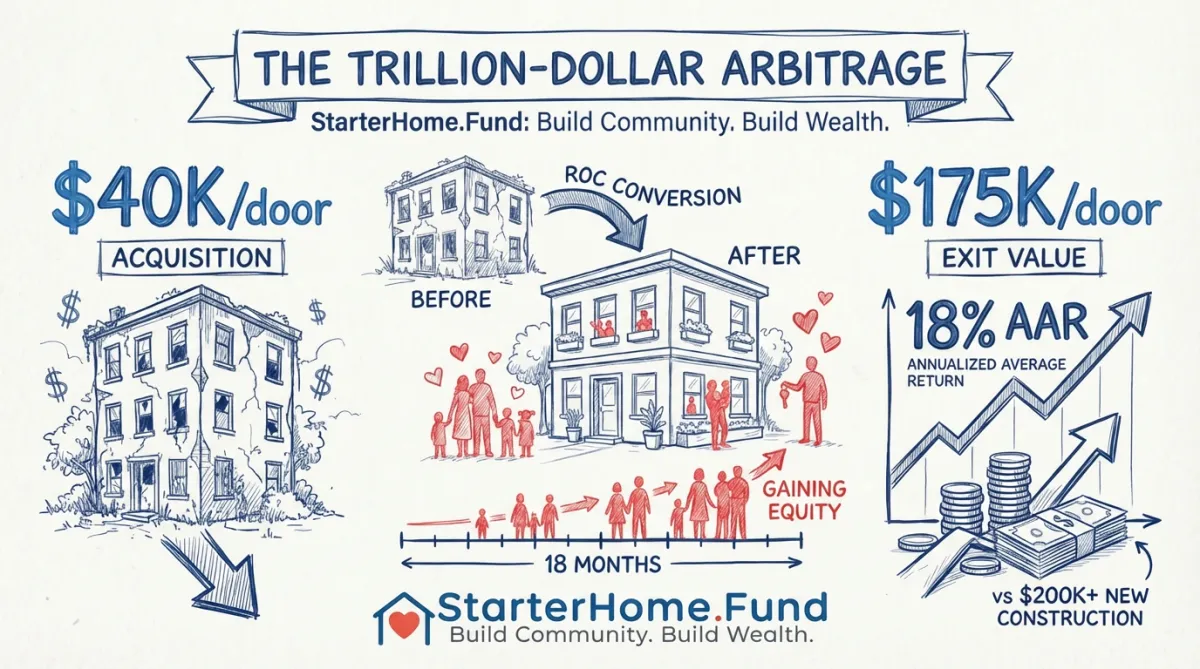

Properties trading at $40K/door in markets where new construction costs $200K/door. This isn't a deal. It's a structural mispricing that won't last.

The Market That Everyone's Ignoring

While every real estate investor in America is chasing:

Luxury apartment conversions

STR properties in vacation markets

Fix-and-flip in hot suburbs

Class A multifamily in growth cities

A $1 trillion+ opportunity is sitting in plain sight, completely ignored.

Distressed affordable housing.

Not because it's a bad investment. Becausenobody's looking at it through the right lens.

The Numbers That Make No Sense

Let me show you the arbitrage:

New Construction Costs (per door):

Urban core markets: $350K-$500K/door

Suburban markets: $200K-$300K/door

Tertiary markets: $150K-$200K/door

Distressed Affordable Multifamily Acquisitions:

Nonprofit properties in foreclosure: $40K-$60K/door

LIHTC properties that can't refinance: $50K-$80K/door

Class C multifamily with deferred maintenance: $60K-$90K/door

You're buying at 20-30% of replacement cost.

In what world is that not an arbitrage opportunity?

Why Nobody Else Sees It

Traditional investors look at distressed affordable housing and see:

❌ Low rents (can't raise them much)

❌ Deferred maintenance (capital intensive)

❌ Difficult tenants (higher management costs)

❌ Regulatory constraints (LIHTC rules, affordability covenants)

❌ Low exit multiples (cap rates in the 7-9% range)

So they pass.

And that's whythe opportunity exists.

The Model They're Missing

What if you're not trying to maximize rents?

What if you're not trying to flip to another landlord?

What if your exit strategy isresident ownership?

The ROC Conversion Model:

Step 1: Acquisition

Distressed 100-unit property in foreclosure

Acquisition price: $4.5M ($45K/door)

Built-in equity: Property worth $12-15M stabilized

Step 2: Stabilization

ROC conversion: Residents become equity owners

Deferred maintenance addressed (residents have skin in the game)

Zero turnover (owners don't move)

Property management costs drop (owners self-manage)

Step 3: Exit

Conservative valuation: $175/door = $17.5M

18-month hold

Returns: 18% AAR

But here's the key:Your exit isn't to another landlord charging max rents. Your exit is tothe residents as owners.

Why This Works Now (And Won't Forever)

Three forces are creating the opportunity:

1.Nonprofit Funding Collapse

DOGE cut 72% of affordable housing nonprofit funding this year.

Properties that were barely surviving on subsidies are now in foreclosure.90,000 LIHTC units are being lost annually.

These aren't bad properties. They're properties caught in a funding crisis.

Result:Acquisitions at $40K-$60K/door

2.Refinancing Cliff

Thousands of affordable housing properties financed at 3-4% rates between 2010-2021 are hitting their refinance windows.

New rates: 6-8%.

Many can't cover the debt service at current rents.

Result:Distressed sales below replacement cost

3.Median Income Crisis

Remember the data:

7.5M affordable units lost in 10 years

Median home requires $103K income (median earns $75K)

Price-to-income ratios at 5.7x

Traditional homeownership is dead for median earners.

But they still want ownership. They still want equity. They still want stability.

ROC conversions provide that.

The Competitive Moat

Here's why this opportunity has staying power:

Most investors can't do this deal.

Why?

They don't understand mission-aligned capital structures

Traditional lenders don't finance ROC conversions

You need access to CDFI loans, social impact capital, and patient money

They don't have the operational expertise

Converting to resident ownership isn't just paperwork

It's community organizing, legal structuring, and cultural change

They're chasing higher rents, not stable communities

Traditional model: maximize rent, minimize services

ROC model: stabilize community, preserve affordability

That complexity is your moat.

The Risk Profile

Let's be honest about the risks:

What could go wrong:

Deferred maintenance costs exceed projections (scope creep)

Resident conversion takes longer than 18 months (timeline risk)

Exit valuations come in below $175/door (market risk)

How we mitigate:

Conservative underwriting: Cap deferred maintenance at 25% of acquisition

Pre-conversion community buy-in: Start organizing before close

Multiple exit strategies: ROC preferred, but can also sell to mission-aligned operators

What's the worst case?

You bought at $45K/door in a market where new construction costs $200K/door and comparable sales are $120K+/door.

Even if the ROC conversion fails,you're sitting on 60%+ built-in equity.

The Scale of the Opportunity

How big is this market?

90,000 LIHTC units failing annually

Thousands of nonprofit properties in foreclosure

100,000+ Class C multifamily units trading below replacement cost

At $50K/door average acquisition, that's$10+ billion in annual deal flow.

And almost nobody is competing for it.

Why It Won't Last

This opportunity has a shelf life.

Eventually:

Social impact capital will wake up to the returns

Traditional PE will figure out the ROC model

Policy will change to rescue failing nonprofits

Replacement cost gap will narrow

The window is now.

Properties are in foreclosuretoday. Nonprofits are losing fundingtoday. The refinancing cliff is happeningnow.

By 2027-2028, this arbitrage will be widely known. Cap rates will compress. Acquisition prices will rise.

First movers will build portfolios at $40K-$60K/door.

Late movers will pay $90K-$120K/door for the same properties.

The Bottom Line

Distressed affordable housing is trading at20-30% of replacement costin markets where demand is exploding and supply is shrinking.

Everyone else is chasing deals in competitive markets with thin margins.

We're buying properties at $45K/door and exiting at $175/door.

We're delivering 18% AAR while preserving affordable housing and creating resident ownership.

And we're doing it in a market wherealmost nobody is competing.

That's not a deal. That's astructural arbitrage.

And it won't last forever.

👉Join the investors who see what others miss.

Earn 18% AAR in Distressed Affordable Housing →

Data Source: Harvard Joint Center for Housing Studies, State of the Nation's Housing 2025